1 2 3 ACCOUNTING The Basis for Business

1

2

3

ACCOUNTING : The Basis for Business Decisions Lecture - 1 4

. Accounting : Information for Decision Making 5

WHAT IS ACCOUNTING? Accounting: The systematic and comprehensive recording of financial transactions pertaining to a business. 6

WHAT IS ACCOUNTING? Accounting also refers to the process of summarizing, analyzing and reporting these transactions. The Language of Business {as it is the means by which information about an enterprise is communicated to make economic decisions} 7

WHAT IS ACCOUNTING? Accounting is : The Art of • Recording • Classifying • Summarizing and • Communicating the results • Of business transactions • On a certain Date. A means to an end. 8

Concepts Underlying Accounting Measurement § Accounting is an information system that measures, processes, and communicates financial information about a business or other economic entity. 1. An economic entity is a unit that exists independently, such as a business, hospital, or governmental body. 2. Bookkeeping is the process of recording financial transactions and keeping financial records. It is mechanical and repetitive and is usually handled by computers.

consist of the interconnected business")

Concepts Underlying Accounting Measurement 3. Management information systems (MIS) consist of the interconnected business subsystems, including accounting, that provide the information needed to run a business. 4. For accounting purposes, a business organization is a separate entity, distinct not only from its creditors and customers but also from its owners.

Business Transactions 1. Business transactions are economic events that affect a business’s financial position. 2. All business transactions are recorded in terms of money. This concept is called money measure. 3. In international transactions, exchange rates must be used to translate from one currency to another. An exchange rate is the value of one currency in terms of another.

Forms of Business Organization § There are three basic forms of business organization that are recognized as separate entities. I - Sole proprietorship—a business owned by one person § The owner takes all the profits or losses of the business and is liable for all its obligations.

Forms of Business Organization II - Partnership—a business that has two or more owners § The partners share the profits or losses according to a prearranged formula. III - Corporation—a business unit chartered by the state and legally separate from its owners § The owners are called stockholders because their ownership is represented by shares of stock.

14

15

16

Types of Accounting Financial Accounting Providing information about the financial resources, obligations, and activities of an economic entity that is intended for use primarily by external decision makers – investors and creditors. General Purpose (Profit, loss, assets, obligation etc) 17

Types of Accounting Management Accounting Providing information that is intended primarily for use by internal management in decision making required to run the business. Helps in Planning and Control 18

Types of Accounting Tax Accounting Preparation of income tax returns and anticipating the tax effects of business transactions and structuring them in such a way as to minimize the income tax burden. Helps in preparation of Income Tax Return etc 19

Financial and Managerial Accounting § Accounting is usually divided into financial accounting and managerial accounting. - External decision makers use financial accounting to evaluate how well a business has achieved its goals. § These reports, called financial statements, are a central feature of accounting. They report on a business’s financial performance.

Financial and Managerial Accounting § Accounting is usually divided into financial accounting and managerial accounting. - Internal decision makers use information provided by managerial accounting about operating, investing, and financing activities. § It provides managers and employees with information about how they have done in the past and what they can expect in the future.

Importance of Financial Accounting The Primary objectives of financial accounting are : 1. to provide information that is useful in making investment and credit decisions in assessing the amount, timing, and uncertainty of future cash flows, 2. It helps in learning about the enterprise’s economic resources, claims to resources. 22

Importance of Financial Accounting The Primary objectives of financial accounting are : 3. Changes in claims to resources. 4. It is means to an end. 5. It is historical to nature 23

Importance of Financial Accounting The Primary objectives of financial accounting are : 6. It results from inexact and approximate measure of business activity, and 7. It is based on a general-purpose assumption. 24

Importance of Management Accounting The Primary objectives of Management Accounting information are : 1. It is useful to the enterprise in achieving its goals, objects and missions 2. Assessing pas performance and 25

Importance of Management Accounting The Primary objectives of Management Accounting information are : 3. Assessing future decisions; and 4. Evaluating and rewarding decision making performance. 26

Importance of Management Accounting The Primary objectives of Management Accounting information are : 5. Some of the important characteristics of management accounting information are its timeliness 6. Its relationship to decision-making authority, 27

Importance of Management Accounting The Primary objectives of Management Accounting information are : 7. Its future orientation 8. Its relationship to measurement efficiency and effectiveness, and 9. The fact that it is a means to an end. 28

29

ACCOUNTING SYSTEM : The personnel, procedures, devices, and records used by an organization to develop accounting information and communicate that information to economic decision makers. 30

31

Economic Activities Human Activities . Non-Economic Activities Profession Business 32

33

Functions of Accounting System 1. In every Accounting System, the economic activities of the organization are Recoded in the books of accounts. 34

Functions of Accounting System 2. Next, the recorded data are Classified in the system to accumulate sub-total for various types of economic activities. 35

Functions of Accounting System 3. Finally, the information is Summarized in Accounting Repots i. e. designed to meet the information needs of the various decision makers. 36

Financial Reporting and Financial Statements �Internal Information: 1. Balanced Sheet 2. Income Statement 3. Statement of Cash flows �Other Information: • Industry • Competitors • Economy-wide 37

Objectives of External Financial Reporting Balance Sheet Income Statement of Cash Flows The primary financial statements. 38

39

40

Decision Makers: The Users of Accounting Information § The people who use accounting information to make decisions fall into three categories: managers (internal users), outsiders who have a direct financial interest in the business, and outsiders who have an indirect financial interest.

Management, Investors, and Creditors § Management is responsible for ensuring that a company meets its goals of profitability and liquidity. § Investors—owners and stockholders—have a direct financial interest in the success of their companies. § Creditors—those who lend money or deliver goods or services before being paid—are interested mainly in whether a company will have the cash to pay interest charges and to repay the debt on time.

External Users of Accounting Information • Creditors • Owners • Labor unions • Governmental agencies • Suppliers • Customers 43

External Users of Accounting Information • Investors • Creditors • Government Agencies (SECP, SBP, IRS, EPA, Ministries etc. ) • Researchers • Trade associations • General public 44

External Users of Accounting Information • Labor Unions • Suppliers • Customers • Trade Associations • General Public 45

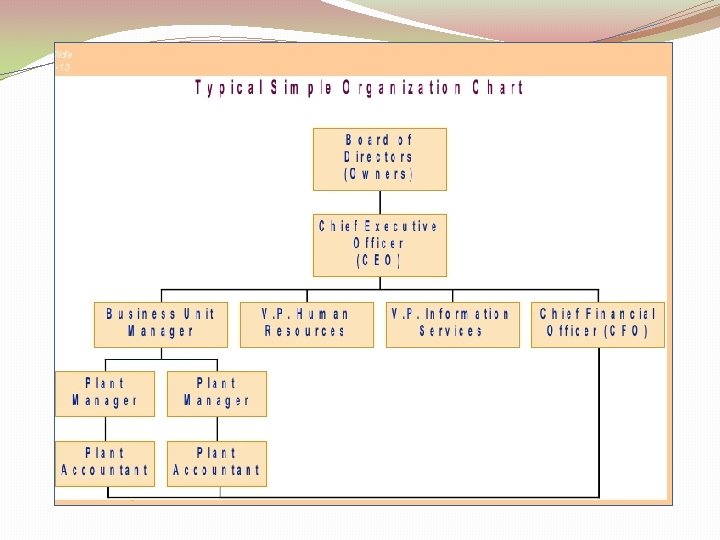

Users of Internal Accounting Information �Board of Directors �Chief Executive Office - CEO �Chief Financial Officer – CFO �Vice Presidents 46

Users of Internal Accounting Information �Business Unit managers �Plant managers �Store Managers �Line Supervisors 47

49

Objectives of Management Accounting Information To help achieve goals and missions To help evaluate and reward decision makers

ŸFinancial Accounting Standards")

Integrity of Accounting Information Institutional Features ŸGenerally Accepted Accounting Principles (GAAP) ŸFinancial Accounting Standards Board ŸSecurities and Exchange Commission ŸInternal Control Structure ŸAudits ŸLegislation

GAAP and the Independent CPA’s Report § To ensure that financial statements are understandable to their users, a set of generally accepted accounting principles (GAAP) has been developed to provide guidelines for financial accounting. § Many companies of all sizes have their financial statements audited by an independent certified public accountant (CPA). �An audit is an examination of a company’s financial statements and the accounting systems, controls, and records that produced them. It ascertains that the statements were prepared in accordance with GAAP.

Organizations That Issue Accounting Standards § Two organizations issue accounting standards that are used in the United States: �The Financial Accounting Standards Board (FASB) has been designated by the Securities and Exchange Commission (SEC) to issue Statements of Financial Accounting Standards. �The International Accounting Standards Board (IASB) issues international financial reporting standards (IFRS). The SEC allows foreign companies to use these standards in the United States.

issues accounting")

Other Organizations That Influence GAAP § The Governmental Accounting Standards Board (GASB) issues accounting standards for state and local governments. § The Internal Revenue Service (IRS) interprets and enforces the tax laws that specify the rules for determining taxable income. § The Public Company Accounting Oversight Board (PCAOB) has wide powers to determine the standards that auditors must follow. .

")

Other Organizations That Influence GAAP § The American Institute of Certified Public Accountants (AICPA) is the primary professional organization of CPAs. § The Securities and Exchange Commission (SEC) is a governmental agency that has the legal power to set and enforce accounting practices for companies whose securities are offered for sale to the general public.

Professional Conduct § The code of professional ethics of the American Institute of Certified Public Accountants governs the conduct of CPAs. The code requires CPAs to act with: �Integrity—be honest and candid and subordinate personal gain to service and the public trust. �Objectivity—be impartial and intellectually honest.

Professional Conduct �Independence—avoid all relationships that impair or appear to impair objectivity. �Due care—carry out professional responsibilities with competence and diligence. § The Institute of Management Accountants (IMA), the primary professional association of managerial accountants, also has a code of professional conduct.

Business Goals and Activities § A business is an economic unit that aims to sell goods and services at prices that will provide an adequate return to its owners. § The two major goals of all businesses are: �Profitability—the ability to earn enough income to attract and hold investment capital �Liquidity—the ability to have enough cash to pay debts when they are due

Integrity of Accounting Information Professional Organizations ŸAmerican Institute of Certified Public Accountants ŸInstitute of Management Accountants ŸInstitute of Internal Auditors ŸAmerican Accounting Association

ŸCertificate")

Integrity of Accounting Information Competence, Judgment and Ethical Behavior ŸCertified Public Accountants (CPAs) ŸCertificate in Management Accounting (CMA) ŸCertificate in Internal Auditing (CIA) ŸCode of Professional Conduct CPA

Integrity of Accounting Information Careers in Accounting ŸPublic Accounting ŸManagement Accounting ŸGovernmental Accounting ŸAccounting Education

SUMMARY ØAccounting is the means by which information about an enterprise is communicated and is called the language of business. ØMany internal and external users have need for accounting information in order to make important decisions. 62

SUMMARY ØBecause the primary role of accounting information is to provide useful information for decision making purposes, it is referred to as a means to an end. ØWith the end being the decision that is helped by the availability of accounting information. 63

64

65

66

- Slides: 66